A stellar employment report, showing that the US added 517,000 jobs in January, threw another wrinkle at investors in early February. Those investors were already digesting interest rate hikes in the US, Eurozone, Canada and the UK, Russian offensives in Ukraine, a mixed 4Q22 corporate earnings season and the latest source of Sino-US friction.

Fears that the strength of America’s labor market will prevent the US Federal Reserve from pivoting from tightening to easing weighed on flows to EPFR-tracked funds, as did the prospect of key geopolitical issues waxing rather than waning. The week ending Feb. 8 saw redemptions from US and China Equity Funds hit year-to-date and 46-week highs, respectively, while Europe Equity Funds saw their longest inflow streak in over a year come to an end.

Overall, Equity Funds posted a collective outflow of $7.4 billion during the first full week of February. Investors also pulled $124 million out of Balanced Funds and $10 billion out of Money Market Funds, with US MM Funds seeing a six-week run of inflows come to an end and China MM Funds recording their biggest inflow in six months. Alternative Funds absorbed $1 billion and Bond Funds $7.4 billion.

At the asset class and single country fund levels, Argentina Equity Funds posted their biggest inflow since late 2Q18 and Vietnam Equity Funds took in fresh money for the 19th consecutive week while Israel Equity Funds notched their biggest outflow in over a year. Mortgage-Backed and Municipal Bond Funds racked up their fourth inflow in the past five weeks, Inflation Protected Bond Funds added to their longest outflow streak since 2013 and investors pulled money from Convertible Bond Funds for the ninth week running.

Emerging Markets Equity Funds

EPFR-tracked Emerging Markets Equity Funds kicked off February with their first outflow since mid-December as concerns about Indian markets, renewed Sino-US tensions and questions about the ceiling for US and European short-term interest rates prompted investors to revisit some of their recent assumptions.

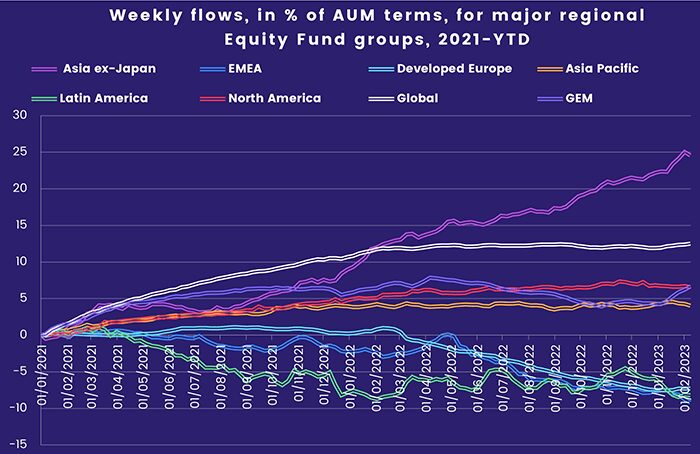

The diversified Global Emerging Markets (GEM) Equity Funds recorded their fifth straight inflow and Frontier Markets Equity Funds took in fresh money for the 15th week in a row. But this was offset by redemptions from Asia ex-Japan, Latin America and EMEA Equity Funds. Overall, EM Equity ETFs posted their first collective outflow since mid-December and their biggest since mid-2Q22.

The shooting down of a Chinese high altitude balloon in US airspace reminded investors that relations between the US and China remain tense, and that economic policy in both countries is currently focused on reducing dependence on the other. China Equity Funds chalked up their biggest outflow in over 10 months despite a sixth straight week of retail inflows. It was also a rough week for dedicated India Equity Funds as the allegations surrounding conglomerate Adani’s bookkeeping – strongly denied by the company – kept investors on edge…

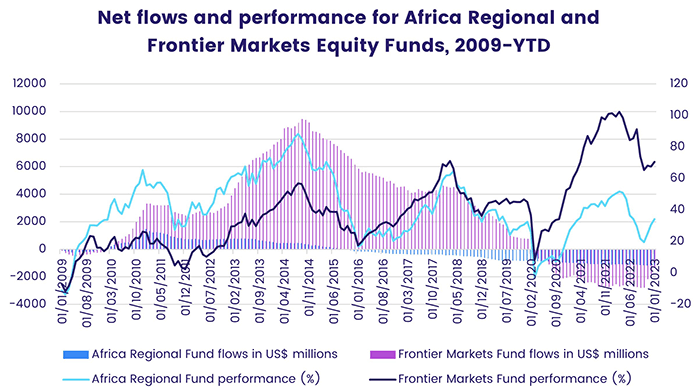

The latest flows into Frontier Markets Equity Funds extended their longest inflow streak in over eight years. Vietnam remains front and center in the latest surge: dedicated Vietnam Equity Funds have absorbed over $1 billion during the past four months and the average Frontier Markets Equity Fund is allocating a fifth of their portfolio to Vietnamese stocks.

Interest in Africa remains at a low ebb, with Africa Regional Equity Funds posting outflows 14 of the past 20 weeks. Other EMEA fund groups are also struggling to attract money for a wide range of reasons. These include funds dedicated to Russia (conflict with Ukraine), Turkey (politics, earthquake), Egypt (debt, inflation) and South Africa (drought, corruption). During the latest week Egypt Equity Funds recorded their biggest outflow since 2012 and Turkey Equity Funds’ current redemption streak hit five weeks and over 12% of their AUM.

Developed Markets Equity Funds

Flows into EPFR-tracked Developed Markets Equity Funds ran into a wall of worry in early February as investors struggled to square the latest American job numbers with their hopes of an early return to lower US interest rates. US Equity Funds posted their fourth outflow year-to-date, the longest inflow streak for Europe Equity Funds since 1Q22 came to an end and Japan Equity Funds saw over $1 billion flow out, more than offsetting flows into Australia, Pacific Regional and Global Equity Funds.

Global Equity Funds, the largest of the diversified Developed Markets Equity Fund groups, took in fresh money for the sixth consecutive week. Global ex-US Funds absorbed more money than their fully global counterparts for the first time since late October. Their latest inflow was the biggest since the second week of 2Q22.

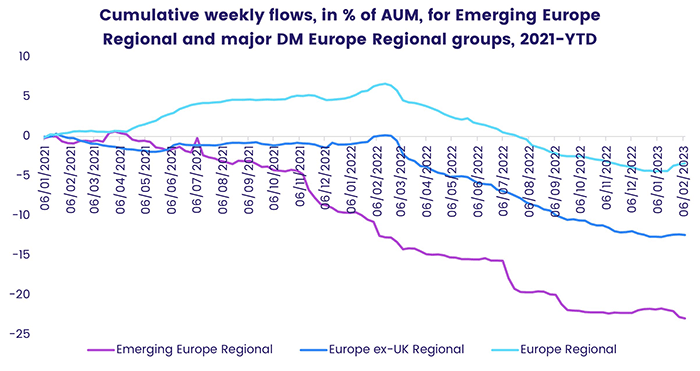

The week ending Feb. 8 including 0.5% interest rate hikes by the Bank of England and the European Central Bank, and Russian troops grinding forward in eastern Ukraine, prompting investors to pull over $350 million out of both France and UK Equity Funds. Retail redemptions from all Europe Equity Funds climbed to an eight-week high and funds with socially responsible (SRI) or environmental, social and governance (ESG) mandates posted their second outflow of 2023.

US SRI/ESG Equity Funds also posted their second outflow year-to-date as retail flows turned negative again. Funds domiciled outside the US recorded their biggest outflow since the first week of September. Flows into Small Cap Value, Growth and Blend and Large Cap Growth Funds hit six to eight-week highs.

Fears that rising domestic wages and inflation, higher US interest rates and speculative pressure on the Bank of Japan’s yield control policies will combine to force a shift in Japanese reliably accommodative monetary policies later this year kept many investors on the sidelines. Japan Equity Funds saw over $1 billion flow out for the second time in the past three weeks.

Global Sector, Industry and Precious Metals Funds

With investors weighing the implications of more interest rate hikes in key developed markets, the unexpectedly strong US labor market, more 4Q22 earning reports and number of geopolitical markers, the first week of February was a choppy one for EPFR-tracked Sector Funds. Only three of the 11 major groups posted an inflow.

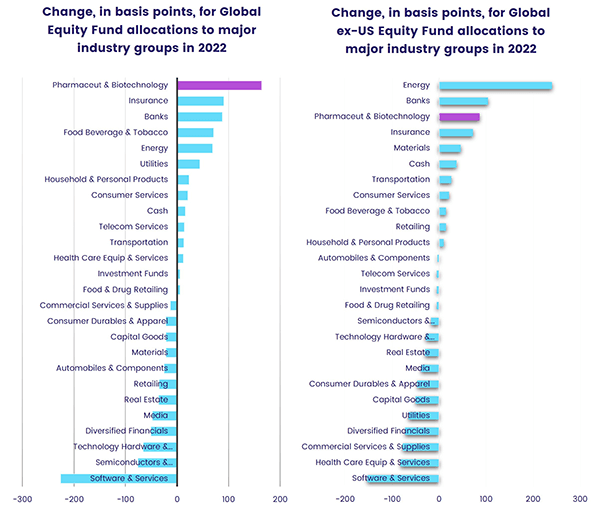

Energy and Healthcare/Biotechnology Sector Funds experienced the heaviest outflows. In the case of the former, which posted their 11th outflow in the past 12 weeks, uncertainty about future demand and fears that the eye-catching profits generated in the final three months of last year will fuel fresh demands for windfall taxes sapped investor appetite. Healthcare/Biotechnology Sector Funds, meanwhile, have now recorded outflows six of the past seven weeks even though industry allocations data shows that Global Equity Fund managers rotated significant exposure to biotechnology and pharmaceutical plays in 2022.

Among the groups recording inflows, Technology Sector Funds snapped their longest outflow streak since 1H07 with the latest inflow the biggest in nearly three months. Moves by major US names to control costs and broad excitement about the potential of artificial intelligence chatbot tools are among the drivers of the renewed appetite for exposure to the technology sector.

Flows to Financial Sector Funds continued their recent rebound, with the group taking in over $1 billion as they extended their longest run of inflows since mid-3Q22. But interest in traditional stores of value remains muted as Gold Funds chalked up their fifth straight outflow.

Redemptions from Utilities Sector Funds climbed to a nine-week high and the group posted consecutive weekly outflows for the first time since mid-November.

Bond and other Fixed Income Funds

Another round of rate hikes in major developed markets, a deeply inverted US sovereign yield curve and fears that Japanese monetary policymakers may not be able to hold their current positions did not stop EPFR-tracked Bond Funds from starting February with their sixth straight inflow.

Of the major groups by geographic focus, only Europe Bond Funds recorded an outflow. Global and Emerging Markets Bond Funds extended their longest inflow streaks since 3Q21 and 2Q21, respectively, while flows into Asia Pacific Bond Funds climbed to a 16-week high. Year-to-date, US Bond Funds have attracted the largest amount of fresh money, Europe Bond Funds have seen the largest retail inflows and Emerging Markets Bond Funds have turned in the best collective performance.

At the asset class level, Total Return Funds chalked up their biggest weekly inflow in over two years, Mortgage-Backed Bond Funds posted consecutive inflows for only the third time since 4Q21 and High Yield Bond Funds took in fresh money for the fourth time in the past five weeks.

Europe Bond Funds saw their latest inflow streak come to an end during a week when the European Central Bank hiked its base interest rate by another 50 basis points and signaled a hike of similar magnitude is likely in March. At the country level, Germany Bond Funds experienced net redemptions for the sixth time in the past eight weeks, posting their biggest outflow since mid-4Q16 when global debt markets were pricing in the economic agenda of US President-elect Donald Trump.

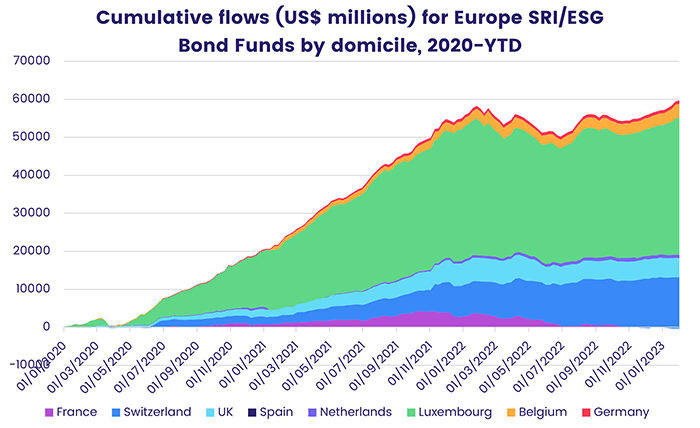

Funds with socially responsible (SRI) or environmental, social and governance (ESG) mandates remained buoyant, posting their 17th straight inflow. Europe SRI/ESG Bond Funds domiciled in Luxemburg and Switzerland have attracted the biggest inflows over the past three years.

Flows into Emerging Markets Bond Funds favored funds with hard currency mandates over their local currency counterparts by a 2-to-1 margin as China Bond Funds racked up their 49th outflow over the past 52 weeks. Long term was the preferred duration, with flows into Long Term EM Funds hitting a 21-week high, and the recent preference for sovereign exposure eased.

US Bond Funds took in over $3.5 billion for the week, with the biggest share of the headline number finding its way into Intermediate Term Mixed, Long Term Treasury and Total Return Funds.

Among the Asia Pacific Country Bond Fund groups, flows into Australia Bond Funds hit a 16-week high and Japan Bond Funds recorded their first inflow since the final week of 2022.

Did you find this useful? Get our EPFR Insights delivered to your inbox.