With the one-year anniversary of Russia’s attack on Ukraine looming, the latest US inflation data showing headline inflation down and core inflation up, the Bank of Japan weeks away from a change in leadership and Sino-US tensions rising, investors found it hard during the second week of February to sustain their earlier optimism. Flows into EPFR-tracked Bond Funds came in lower for the fifth week running, collective flows to all Equity Funds totaled $324 million and seven of the 11 major Sector Fund groups experienced net redemptions.

Funds with socially responsible (SRI) or environmental, social and governance (ESG) mandates continue to provide comfort, with SRI/ESG Equity Funds pulling in $2.87 billion and SRI/ESG Bond Funds close to $2 billion.

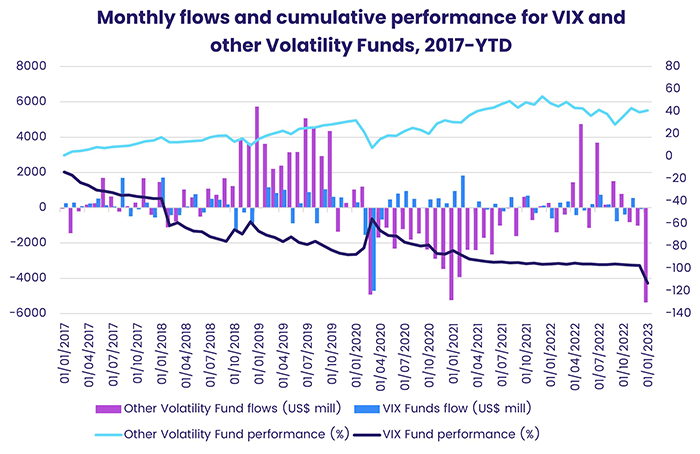

The uncertainty has not, so far, pushed investors into Volatility Funds. Funds dedicated to the VIX index posted their eighth outflow in the past 10 weeks and redemptions from other Volatility Funds climbed to a level last seen in mid-2Q21.

Overall, the week ending Feb. 15 saw Bond Funds pull in another $5.4 billion, with Alternative Funds attracting $1.2 billion and Money Market Funds $1 billion while a net $1 billion flowed out of Balanced Funds as they posted their 25th outflow in the past 27 weeks.

At the single country and asset class fund levels, Cryptocurrency Funds chalked up their biggest outflow since mid-3Q22 and redemptions from High Yield Bond Funds exceeded $3 billion while Convertible Bond Funds snapped a nine-week outflow streak. Flows into Switzerland, Austria and Greece Equity Funds hit 33, 43 and 53-week highs, respectively, and Korea Bond Funds posted their 13th consecutive inflow.

Emerging Markets Equity Funds

Investors retained their appetite for diversified exposure to emerging markets equity during the week ending Feb. 15. That was enough to offset the headwinds generated by fears that the US interest rate cycle has further to run, Russia’s latest offensives in Ukraine and the shift for worse in Sino-US relations. EPFR-tracked Emerging Markets Equity Funds posted their eighth inflow in the past nine weeks as EM Dividend Equity Funds extended their longest inflow streak since 4Q21 and funds with socially responsible (SRI) or environmental, social and governance (ESG) mandates took in fresh money for the 13th week in a row.

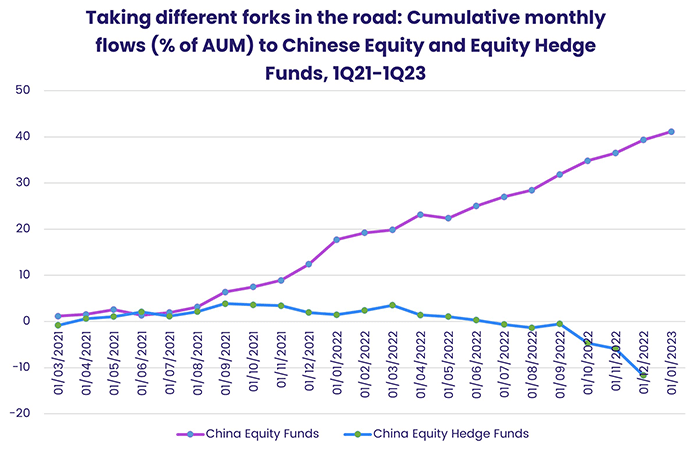

Despite the recent rebound in retail flows, China Equity Funds posted their first consecutive weekly outflows since the second quarter of last year, threatening a streak that has seen them post eight consecutive monthly inflows. Meanwhile, Hedge Funds dedicated to Chinese equity saw redemptions accelerate coming into 2023.

Among Asia ex-Japan Country Fund groups dedicated to smaller markets, Thailand Equity Funds snapped a six-week run of outflows and Vietnam Equity Funds extended their current inflow streak to 20 straight weeks. In the case of Thailand, a slow but steady increase in tourist visits is boosting the country’s economy while Vietnam’s economic growth and supply chain relocation story continue to attract attention.

EMEA Equity Funds recorded their fifth straight outflow as the devastating earthquake that hit Turkey earlier in the month added to the headwinds facing a group that also encompasses Russia, Ukraine, Egypt and Nigeria. During the latest week, Kuwait Equity Funds posted their biggest inflow since 4Q20 and funds dedicated to the Slovak Republic attracted more fresh money.

Brazil Equity Funds recorded the biggest inflow among the major Latin America Equity Fund groups as investors responded to the plateauing of Brazilian interest rates and the prospect of increased Chinese demand for the country’s commodity exports. But redemptions from Mexico Equity Funds jumped to a nine-week high after January’s inflation number prompted the Bank of Mexico to increase its key interest rate to a 15-year high.

Developed Markets Equity Funds

Going into the second half of February, EPFR-tracked Developed Markets Equity Funds struggled to attract fresh money for the second week running as a clear fix on the nexus between peak US interest rates and slowing global growth continued to elude investors. Flows into Global, Europe, Canada and Australia Equity Funds did, narrowly, offset redemptions from US, Japan and Pacific regional Funds.

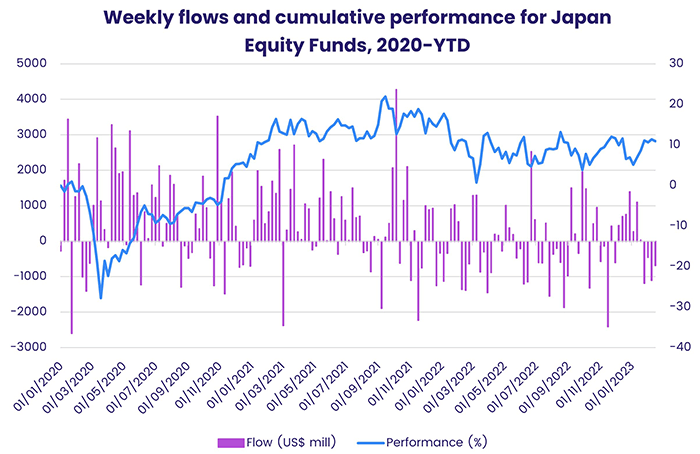

Japan Equity Funds extended their longest outflow streak since the third quarter of last year as markets look ahead to the end of April when current Bank of Japan Governor Kuroda Haruhiko steps down, with Ueda Kazuo his likely replacement. The combination of higher interest rates overseas, domestic inflation running at 4% and speculative pressure on the BOJ’s yield control policies suggest that the central bank will have to start ‘normalizing’ its ultra-accommodative policies later this year.

In the US, normalization of monetary policy has now been underway for nearly 11 months. Hopes that one more hike will take interest rates to their peak level have been dented by January’s strong job creation and retail sales, and the rise in core inflation. US Equity Funds recorded their fifth outflow year-to-date as retail redemptions climbed to a nine-week high and US Dividend Equity Funds racked up their fourth outflow in the past five weeks.

Europe Equity Funds posted their fourth inflow in the past five weeks as the benchmark EuroStoxx 600 index hit a 14-month high. Solid flows into regional and dedicated Switzerland Equity Funds underpinned the week’s headline number, offsetting the drag from Germany, France and UK Equity Funds. The latter posted their sixth straight outflow and 32nd in the past 34 weeks as investors weighed the latest drop in Britain’s inflation rate against the fact it is still north of 10%.

The largest of the diversified Developed Markets Equity Fund groups, Global Equity Funds, extended their current inflow streak to seven weeks and $9.4 billion.

Global Sector, Industry and Precious Metals Funds

The week ending Feb. 15 was marginally better for EPFR-tracked Sector Funds, with four recording inflows versus three the previous week. But geopolitical issues, rising interest rates and gloomy earnings guidance for the next two quarters continued to take their toll on investor sentiment.

Financials Sector Funds were, again, the biggest money magnets, extending their current run of inflows to four weeks and $2.75 billion. Among the 10 funds reporting the biggest inflows for the week, three were bank focused, three were securities related and one had an insurance mandate. Despite this, Insurance Funds added to their 31-week redemption streak.

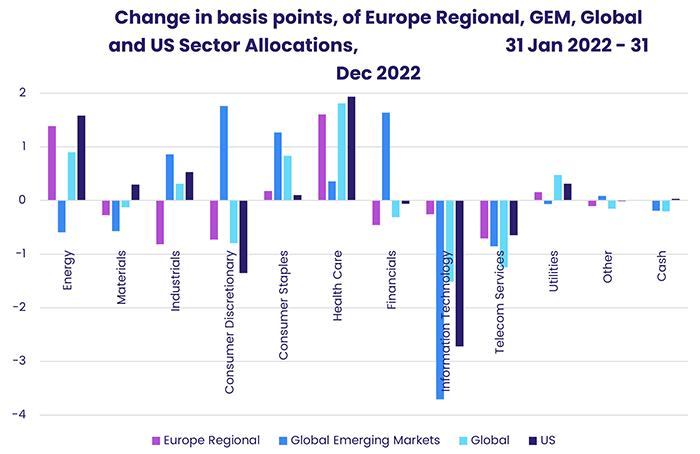

Investors have pulled money out of Healthcare/Biotechnology Sector Funds for the past four weeks, with dedicated Biotechnology Funds underpinning the headline number. Last year, as the chart below highlights, several fund groups rotated exposure from other sectors to healthcare plays.

Despite hopes for increased Chinese demand in the second half of the year, both Commodities and Energy Sector Funds experienced net redemptions with the latter seeing over $1 billion flow out for the second straight week. Copper Funds, however, posted their biggest weekly inflow on record and dedicated Natural Gas Funds chalked up their eighth inflow in the past nine weeks.

Technology Sector Funds also recorded an outflow of $1 billion, their biggest since early November, as funds dedicated to China posted their biggest outflow in over six months against a backdrop of rising Sino-US tensions.

Bond and other Fixed Income Funds

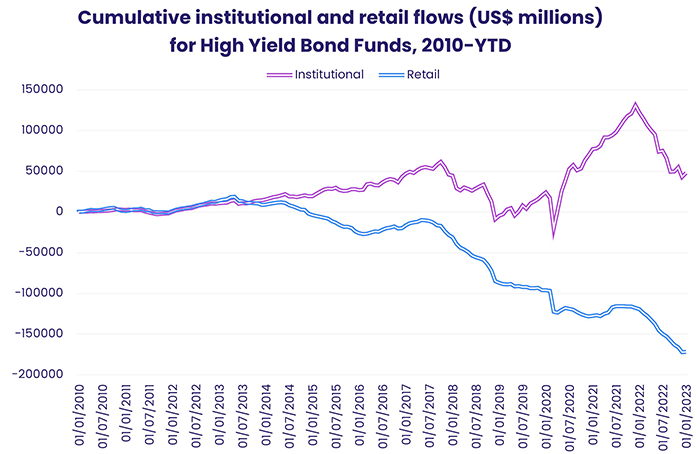

EPFR-tracked Bond Funds kept their current inflow streak alive during the second week of February, although investors took steps to cut risk as Russia’s attack on Ukraine moved closer to the one-year mark, core inflation in the US climbed and markets digested a flood of new issuance. Redemptions from High Yield and Emerging Markets Bond Funds hit eight and 14-week highs, respectively, and Bank Loan Funds posted their 35th outflow in the past eight months.

In addition to immediate challenges, some issues with longer fuses are beginning to occupy fixed investors. These include the prospect of another partisan game of brinkmanship over the US debt ceiling and the sunsetting of the London Inter-Bank Offered Rate (Libor) that was widely used to price debt for nearly five decades.

Among the major groups by geographic focus, flows into Global Bond Funds took in fresh money for the eighth week running, Europe Bond Funds recorded their sixth inflow year-to-date and US Bond Funds extended their longest inflow streak since 3Q21.

Both Hard and Local Currency Emerging Markets Bond Funds saw money flow out during the week ending Feb. 15, and redemptions from Frontier Markets Bond Funds hit a 17-week high. Coming into 2023, the latter’s allocations to Ethiopia, Mozambique and Iraq were at their highest levels in over five years.

US Bond Funds experienced their heaviest retail redemptions since mid-December but flows into funds with socially responsible (SRI) or environmental, social and governance (ESG) mandates climbed to a 53-week high. Investors favored US Sovereign Bond Funds over their corporate counterparts and Intermediate over Short- and Long-Term Funds. Foreign domiciled funds absorbed more than double the amount of fresh money committed to funds based in the US.

Among Europe Bond Fund groups, those with corporate mandates recorded their 18th consecutive inflow and Europe Inflation Protected Bond Funds their ninth consecutive outflow. Italy Bond Funds posted their biggest outflow since early September, UK Bond Funds took in fresh money for the 14th straight week and investors pulled another $97 million out of Germany Bond Funds.

Did you find this useful? Get our EPFR Insights delivered to your inbox.