Investors hoping for the p-word got one during the third week of September. But it was ‘plateau’, rather than ‘pivot’, as the Bank of England and US Federal Reserve kept interest rates at their current levels but went out of their way to stress that they could remain at those levels for some time.

The week ending September 20 did see some better Chinese macroeconomic data, and China Equity Funds rebounded from two consecutive outflows with a $2.5 billion inflow. But two-thirds of the money committed to US Equity Funds the previous week flowed back out and UK Equity Funds accounted for a third of the headline number for all Europe Equity Funds as they extended their current redemption streak.

Overall, EPFR-tracked Equity Funds posted a collective outflow of $16.9 billion during the third week of September. Investors also pulled $3.2 billion out of Balanced Funds and $4.2 billion out of Money Market Funds while Alternative Funds absorbed a net $938 million and Bond Funds $2.5 billion.

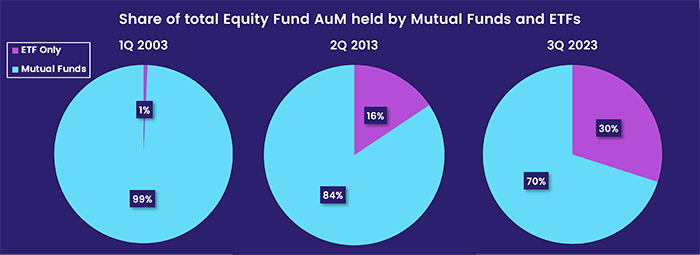

Exchange Traded Funds (ETFs) continue to expand their footprint. Among Equity Funds, they have doubled their share of the total asset pie over the past decade while Bond ETFs now hold nearly 25% of the total AUM for all Bond Funds.

At the asset class and single country fund level, the week ending Sept. 20 saw Derivatives Funds post a record-setting inflow, money flow out of Gold Funds for the 17th consecutive week, Inflation Protected Bond Funds chalk up their 50th outflow over the past 12 months and High Yield Bond Funds‘ three-week run of inflows come to an end. Redemptions from Colombia and Qatar Bond Funds hit 14-week and record highs, respectively, while Singapore Equity Funds posted their biggest inflow in nearly three months.

Emerging markets equity funds

Evidence that policy measures are giving China’s lackluster economic rebound a shot in the arm helped China Equity Funds snap their longest outflow streak since mid-April and allowed all EPFR-tracked Emerging Markets Equity Funds to post inflows for the 29th time in the 38 weeks year-to-date. But the diversified Global Emerging Markets (GEM) Equity Funds experienced net redemptions for the eighth week running, and retail share classes saw money flow out for the seventh straight week.

Viewed by domicile, EM Equity Funds based in Japan chalked up their 37th consecutive inflow while Europe-domiciled funds recorded their 10th outflow in the past 12 weeks.

The third week of September was another good one for EM Dividend Funds, which took in over $500 million for the second week running.

Data for August that showed improvements in bank lending, retail sales and industrial production boosted sentiment towards China, with China Equity Funds taking in over $2 billion for the seventh time quarter-to-date and 18th time year-to-date. India Equity Funds continue to post above average inflows, with the latest week seeing their current inflow streak hit 28 weeks and over $15 billion total, as the country moves closer to displacing Germany as the world’s fourth-largest economy.

China’s latest data also gave Brazil’s export story a welcome boost. Flows into Brazil Equity Funds rebounded to a five-week high while both Mexico and Colombia Equity Funds posted outflows that, in the case of the latter, were the biggest in over 11 months.

With the latest production cuts from Saudi Arabia and Russia keeping oil prices pegged around the $90 a barrel mark, flows into Saudi Arabia Equity Funds climbed to their highest level since early 2Q22. There was less enthusiasm for oil importers within the EMEA universe, with Turkey Equity Funds seeing over 1% of their AUM redeemed and Poland Equity Funds chalking up their ninth outflow during the past 10 weeks.

Developed markets equity funds

With oil prices climbing and major central banks preaching continued vigilance against rising prices, the third week of September was a tough one for EPFR-tracked Developed Markets Equity Funds. Investors pulled significant sums from US and Europe Equity Funds, and more modest sums from Canada and Pacific Regional Equity Funds, which far exceeded the collective flows into Global, Japan and Australia Equity Funds.

The latest flows into Japan Equity Funds came ahead of the Bank of Japan’s September policy meeting, which is expected to leave current policies unchanged but give more clues about the pace – and degree – of policy normalization that markets expect next year. Foreign-domiciled Japan Equity Funds posted their 23rd inflow over the past 25 weeks. But funds with socially responsible (SRI) or environmental, social and governance (ESG) mandates posted consecutive weekly outflows for the first time since early February, with the latest redemptions the largest in 11 weeks.

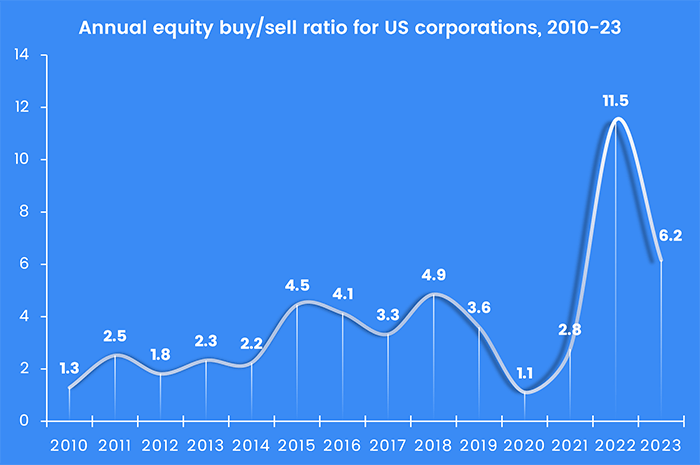

US Equity Funds saw over $17 billion flow out during a week that ended with the US Federal Reserve keeping interest rates on hold but sending a clear higher-for-longer signal. Research by EPFR Liquidity Analyst Winston Chua also shows that the extraordinary support of their own stock prices by US corporations is losing momentum. While they are still shrinking their free float, the ratio of buying to selling new shares has fallen by nearly half over the past year.

With investors still digesting last week’s 25 basis point rate hike by the European Central Bank and unsure how soon the Bank of England can pivot to an easing stance, redemptions from Europe Equity Funds accelerated for the second week running. At the country level, investors pulled over $1 billion from UK Equity Funds while redemptions from Spain and Greece Equity Funds hit 13 and 27-week highs, respectively.

Global Equity Funds, the largest of the diversified Developed Markets Equity Fund groups, posted their fourth straight inflow. There was little difference between the flows into Global ex-US Equity Funds and those going to funds with fully global mandates.

Global sector, industry and precious metals funds

With the 3Q23 earnings season only three weeks away and monetary policy generally on hold or, in the case of emerging markets, easing, sector-oriented investors became more active going into the final 10 days of September. Those investors committed fresh money to five of the 11 major EPFR-tracked Sector Fund groups, up from two the previous week, with inflows ranging from $45 million for Infrastructure Sector Funds – a 10-week high – to $1.2 billion for Technology Sector Funds.

Although they didn’t record the biggest collective inflow, Energy Sector Funds were the group that stood out during the third week of September. Against a backdrop of speculation that oil prices will make a run at the $100 a barrel mark, flows into a group that posted 13 consecutive outflows between mid-April and mid-July hit a 48-week high.

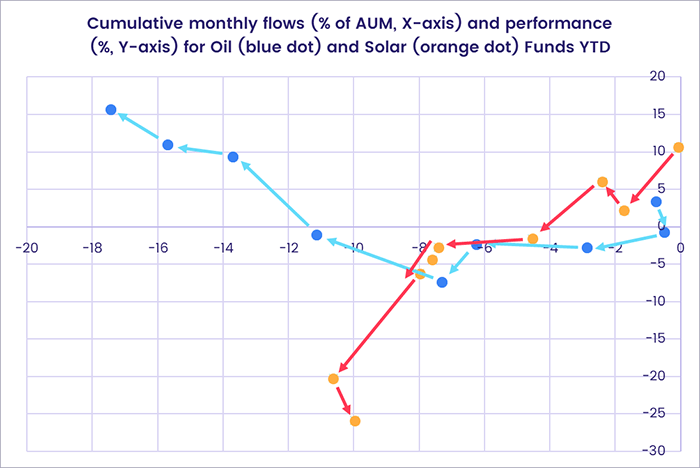

Drilling down, investors have taken a keen liking to a few Energy Sector Fund subgroups this year. Natural Gas Funds have absorbed $2.1 billion (or 67% of assets) and flows into Nuclear & Uranium Funds have pushed past the $500 million mark. But two groups at opposite ends of the green energy spectrum have been among the hardest hit. Year-to-date, Oil and Solar Funds have seen outflows hit $6 billion (21% of assets) and $293 million (10% of assets), respectively.

Elsewhere, Consumer Goods Sector Funds snapped a five-week outflow streak that totaled $1.5 billion. EPFR’s Sector Allocations data shows that US Equity Fund managers have been increasing their exposure to Consumer Discretionary since May, while allocations to Consumer Staples peaked in April and have since cooled off.

Financials Sector Funds suffered their heaviest outflow in seven weeks and the second above $1 billion in their current eight-week outflow streak. Redemptions from US-dedicated funds hit a year-to-date high, investors bailed out of Europe Financials Sector Funds for the 23rd straight week and Korea-dedicated funds saw a record outflow of $53 million. China Financial Sector Funds did enjoy a fourth consecutive week of inflows and Regional Banks Funds saw inflows reach a 15-week high.

Bond and other fixed income funds

Heading into another flurry of central bank meetings, EPFR-tracked Bond Funds extended an inflow streak stretching back to the final week of March. During that run, Bond ETFs have absorbed nearly $3 for every dollar committed to actively managed funds and Sovereign Bond Funds have taken in over $15 for every dollar absorbed by Corporate Bond Funds.

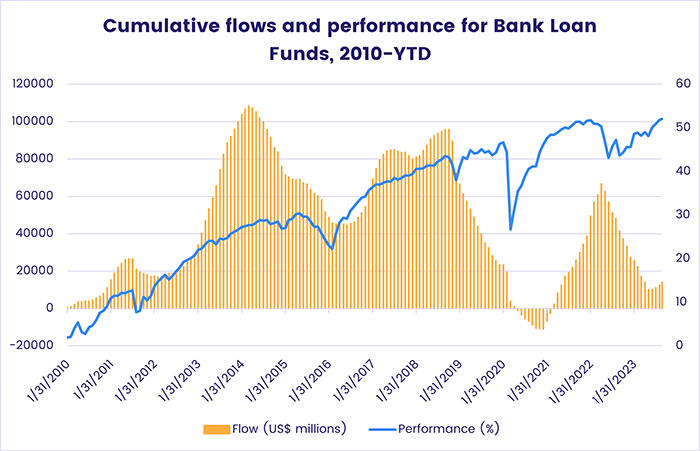

Investors remain leery of the risk/reward profiles offered by junk and emerging markets bonds during the third week of September. They pulled money out of Emerging Markets Bond Funds for the eighth week running and from High Yield Bond Funds for the sixth time in the past nine weeks. But, with a ‘soft landing’ still penciled in for the US economy, there has been no late cycle exodus from Bank Loan Funds. That group has now taken in fresh money for eight consecutive weeks and 14 of the past 16.

Retail investors gravitated to Europe and Global Bond Funds during the latest week, with inflows hitting six and seven-week highs respectively. But redemptions from US Bond Fund retail share classes hit levels last seen in mid-March. That did not stop US Bond Funds overall from extending their current inflow streak to 38 straight weeks as flows into Long Term Corporate Funds climbed to a 13-week high.

For investors seeking exposure to European corporate debt, intermediate was the preferred duration for the fourth straight week. Among Europe Country Bond Fund groups, flows into Spain and Switzerland Bond Funds climbed to 14 and 16-week highs, respectively, and Italy Bond Funds extended their longest run of inflows since EPFR started tracking them in 2012.

Redemptions from Emerging Markets Bond Funds hit hard currency funds harder than their local currency counterparts. Long Term EM Bond Funds recorded modest inflows while outflows from Short Term EM Funds hit a seven-week high, sharia-compliant funds took in fresh money for the ninth time in the past 12 weeks and Frontier Markets Bond Funds chalked up their seventh outflow QTD.

Did you find this useful? Get our EPFR Insights delivered to your inbox.