Record-setting flows into US Equity Funds ahead of the first “quadruple witching” of 2024 for futures and options contracts and February’s inflation data lifted the headline number for all EPFR-tracked Equity Funds to a three-year high during the second week of March.

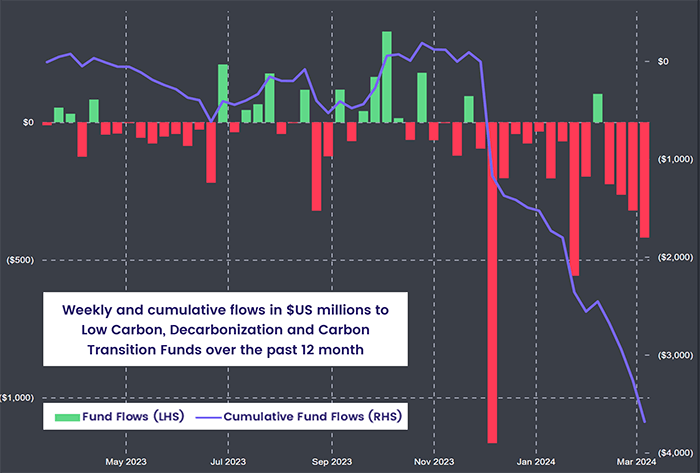

The influx of fresh money did not, however, lift Equity Funds with socially responsible (SRI) or environmental, social and governance (ESG) mandates out of their current flow slump. Investors pulled money out of these funds for the 13th week running, with the latest redemptions hitting an eight-week high, as sub-groups ranging from Electric Vehicle to Decarbonization Funds experienced net redemptions.

With the narrative on the US interest rate cycle shifting again, as inflation in the world’s largest economy overshot forecasts in February and some recent US Treasury auctions attracted lackluster demand, interest in emerging markets assets slumped. But Cryptocurrency Funds set another weekly inflow record and flows into all Alternative Funds climbed to a 103-week high.

Overall, Alternative Funds pulled in a net $3.3 billion during the week ending March 13 while $7.7 billion flowed into Bond Funds, $49.7 billion into Money Market Funds and $55.7 billion into Equity Funds while Balanced Funds saw $3.2 billion flow out.

At the asset class and single country fund levels, Municipal Bond Funds extended their longest inflow streak since 3Q21, flows into Silver Funds climbed to a 61-week high and High Yield Bond Funds chalked up their 19th inflow over the past 20 weeks. Redemptions from Italy Equity, UK Bond and Argentina Equity Funds hit eight, 17 and 21-week highs respectively while Italy Bond Funds recorded their biggest inflow in over seven months and Greece Equity Funds posted their 17th inflow since early November.

Emerging markets equity funds

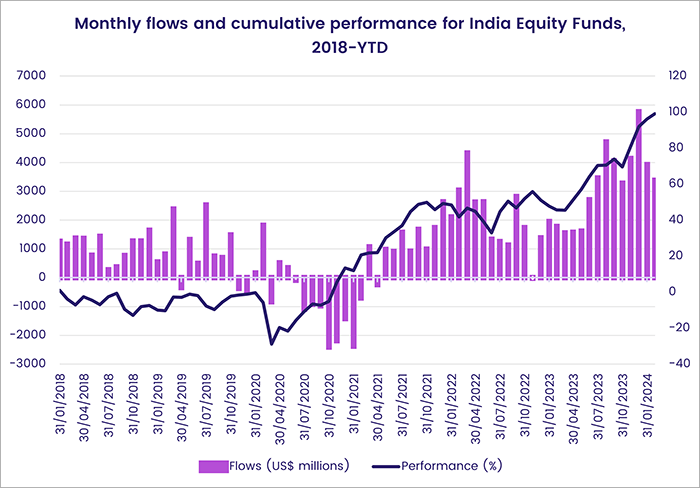

Despite another week of flows into India Equity Funds – their 51st since their current record-setting inflow streak began in late 1Q23 – the prospect of US interest rates staying at their current levels into the second half of this year sapped investor appetite for emerging markets equity going into the third week of March.

All four of the major EPFR-tracked Emerging Markets Equity Funds groups by geographic focus recorded net outflows for the week ending March 13 that ranged from $8 million for EMEA Equity Funds to $450 million for Asia ex-Japan Equity Funds. Retail share classes collectively experienced net redemptions for the 25th time during the past six months. European domiciled EM Equity Funds posted outflows for the 31st consecutive week while funds domiciled in Japan extended an inflow streak stretching back to the fourth week of 4Q22.

Among the Asia ex-Japan Country Fund groups, China Equity Funds posted their second outflow year-to-date as investors continued to digest the Chinese government’s growth target for 2024 – around 5% – and the measures proposed to achieve that target. Funds dedicated to India, which offer exposure to 6% GDP growth and a business-friendly government widely expected to win this year’s general election, chalked up their 51st consecutive weekly inflow.

Other regional groups struggled to attract fresh money, with redemptions from Vietnam Equity Funds climbing to a 17-week high and Thailand Equity Funds extending their longest redemption streak since 3Q22. Korea Equity Funds recorded their fourth straight outflow as North Korea’s bellicose rhetoric, largely articulated by Supreme Leader Kim Jong Un, reached unnerving highs.

Investors pulled money out of Latin America Equity Funds for the ninth time so far this year, with flows to Argentina Equity Funds going into reverse as legislative opposition to new President Javier Milei’s economic agenda stiffened and enthusiasm for Brazil remaining at a low ebb.

In the EMEA universe, investors prospected among the smaller markets during the second week of March. Kuwait Equity Funds recorded their biggest inflow in nearly 13 months and fresh money flowed into Romania Equity Funds for the 19th week in a row.

Developed markets equity funds

A surge of money into US Equity Funds at the end of the latest reporting period saw EPFR-tracked Developed Markets Equity Funds post their biggest collective inflow since late 1Q21 during the second week of March. Japan and Global Equity Funds also contributed to the headline number.

The record-setting flows into US Equity Funds came during a week when key stock indexes hit fresh record highs but ahead of the latest producer price data and the “quadruple witching” expiration of four kinds of derivative contracts. The flows were broadly distributed, with 45 funds taking in over $250 million and 16 of them absorbing over $1 billion. Retail share classes surrendered money for the 24th straight week, but flows into Leveraged US Equity Funds climbed to an 86-week high.

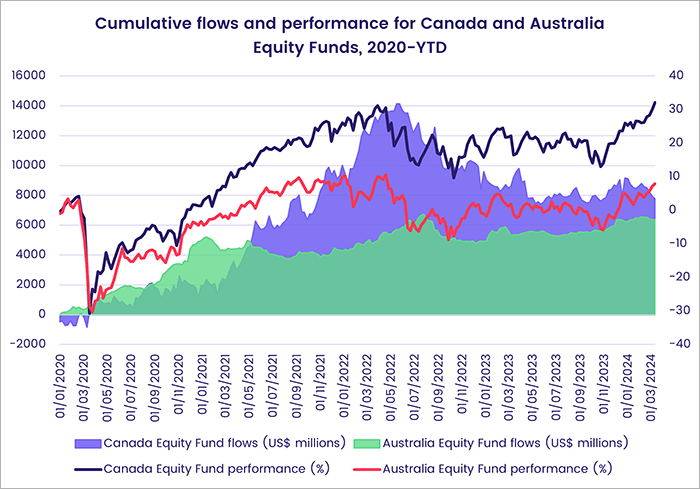

Funds dedicated to America’s northern neighbor did not fare as well, with Canada Equity Funds extending their longest redemption streak since 1Q23. Sentiment towards the other major developed markets resource play has also been weak, although Australia Equity Funds did see a four-week run of outflows come to an end.

Japan Equity Funds posted their ninth straight inflow, but the headline number was a third of the previous week’s total as investors looked ahead to the Bank of Japan’s second policy meeting of the year. Inflation that remains north of the BOJ’s 2% target and some wage agreements boosting wages by over 10%, speculation is mounting (again) that the process of normalizing Japanese monetary policy is about to kick off.

Despite French, German and pan-European indexes testing record highs, Europe Equity Funds saw another $1.7 billion redeemed during the latest week with UK Equity Funds accounting for over a third of that number as they posted their 16th consecutive outflow.

Global Equity Funds, the largest of the major diversified Developed Markets Equity Funds groups, posted their 10th inflow of the year. So far in 2024, funds with ex-US mandates have taken in $5 for every $3 committed to funds with fully global mandates.

Global sector, industry and precious metals funds

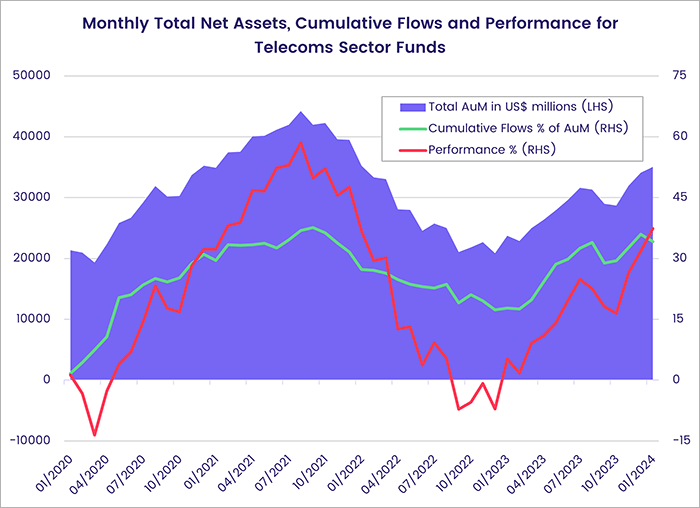

In the aftermath of the 4Q23 earnings season, investors have been looking ahead. They appear to be getting comfortable with what they are seeing. During the second week of March, the number of EPFR-tracked Sector Fund groups reporting inflows – six – outweighed those reporting outflows for the first time in over three months. Technology Sector Funds attracted the biggest inflow since an all-time high of $8.5 billion in May of last year and flows into Telecoms Sector Funds soared to record $1.5 billion.

Telecoms Sector Funds mainly consist of industries related to communication services or devices, but also include entertainment, media, and wireless. With the demand for data picking up, fresh tailwinds from the growth of the metaverse and virtual reality experiences are boosting this universe; total assets for this group have climbed over $15 billion since December 2022 and surpassed the $35 billion mark in January this year.

Collective performance has also been positive, climbing nearly 9% this year despite a net outflow of $460 million during the first month of 2024. But the inflows experienced this week by Telecom Sector Funds reversed that direction of travel, with year-to-date inflows now at 4.1% of assets.

For a second consecutive week, investors pumped over $400 million into Healthcare/Biotechnology Sector Funds. During the height of the Covid pandemic, many put off doctor visits and major surgeries to reduce the risk of infection, but demand for those services has rebounded. Innovations in the drug industry have also boosted investor optimism this year.

Flows into Technology Sector Funds snapped back after last week’s rare outflow, with the group attracting their second-largest inflow since EPFR first started tracking these funds weekly in 3Q00. This brought year-to-date flows past the $20 billion mark, on track to beat the quarterly inflow record of $28.2 billion set in 1Q21.

In addition to funds with telecoms and technology mandates, Industrials Sector Funds are the only other group that has recorded inflows year-to-date.

Silver Funds, with their correlation to industrial and technology sector demand, tend to fare better in relative terms when investors are comfortable with recovery and growth narratives. The group absorbed just their second inflow of the year and fourth since mid-October with the price of the precious metal jumping to around $25 per ounce. The other major precious metals group, Physical Gold Funds, recorded their 11th consecutive outflow.

Bond and other fixed income funds

Although flows into EPFR-tracked Bond Funds paled in comparison to the more than $50 billion absorbed by all Equity Funds, the nearly $8 billion they pulled in during the second week of March lifted their year-to-date total over the $155 billion mark.

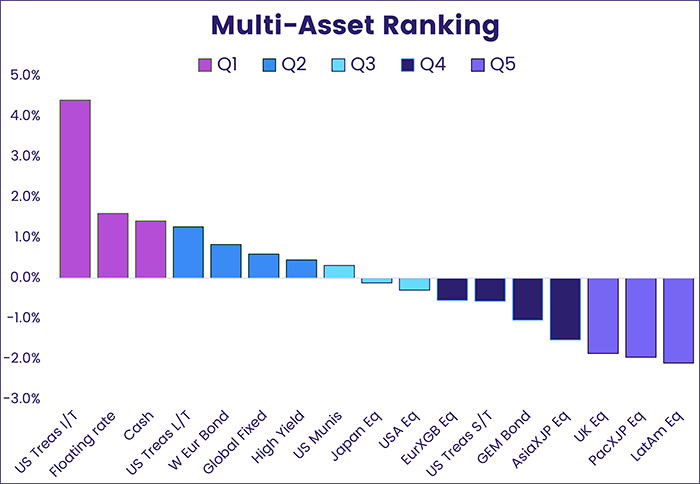

US Bond Funds again pulled in the biggest share of the week’s inflows, and intermediate and long-term Treasuries occupy the top two slots in EPFR’s weekly multi-asset rankings. But overall flows slipped to a six-week low as several US sovereign debt auctions encountered lackluster demand. US Sovereign Bond Funds posted their fourth outflow YTD while US Corporate Bond Funds chalked up their 10th inflow over the same period.

At the asset class level, both floating rate loans and junk bonds remain in the top two quintiles of the weekly rankings. Bank Loan Funds have posted inflows five of the past six weeks and High Yield Bond Funds 19 of the past 21 weeks. In the case of the latter group, investors are showing an increased willingness to take on duration risk. Long Term HY Bond Funds have posted inflows for 10 straight weeks, with flows during the first week of February hitting an eight-month high.

Europe Bond Funds recorded their 19th consecutive inflow, with funds offering exposure to sovereign debt again lagging their corporate counterparts when it came to attracting fresh money. At the country level, redemptions from UK Bond Funds hit their highest level so far this year while flows into Italy Bond Funds climbed to a 33-year high.

A six-week run of inflows came to an end for Japan Bond Funds ahead of the Bank of Japan’s policy meeting during the coming week. Redemptions hit an eight-week high.

Appetite for Emerging Markets Bond Funds remains subdued, although both Hard and Local Currency EM Funds posted modest inflows that were more than offset by outflows from mixed currency funds. China Bond Funds posted their biggest inflow of the year despite yet another major property developer, China Vanke, struggling to stay afloat.

Did you find this useful? Get our EPFR Insights delivered to your inbox.