EPFR started tracking equity fund flows in the first quarter of 1996. It started tracking its first funds with socially responsible (SRI) or environmental, social and governance (ESG) mandates in 2000. But it was not until late 2016 when flows into SRI/ESG Equity Funds really took off.

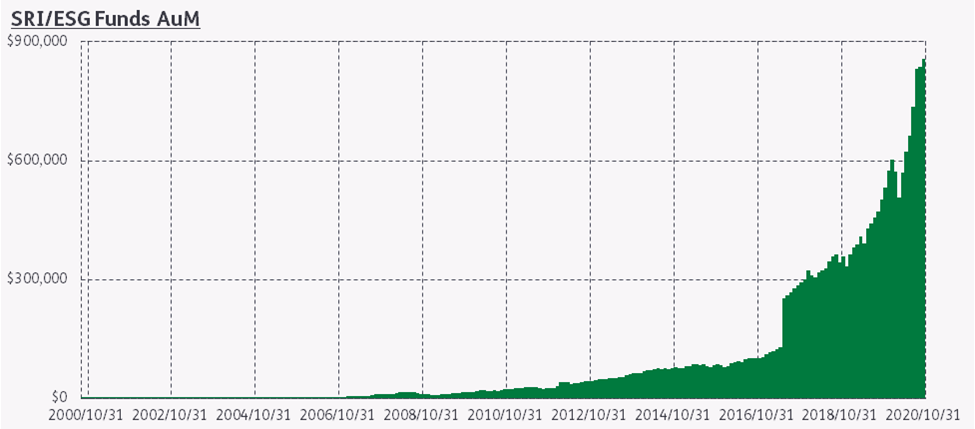

That take off has been followed by astonishing acceleration, both in terms of flows to these funds and the assets they manage. After more than a decade of being incidental, the AUM of SRI/ESG Equity Funds has grown to the point where they represent approximately 4.17% of all the assets managed by all EPFR-tracked Equity Funds (see Chart 1 below).

Chart 1 – SRI/ESG Funds AuM

Since June 2016, ESG funds have only recorded two monthly outflows – September 2016 and January 2017 – and their managers have found themselves consistently entering the market to buy more assets.

Moving the needle – sort of

What is the impact of all this ‘green’ money moving from funds to markets? Does it generate actionable signals that investors can profit from?

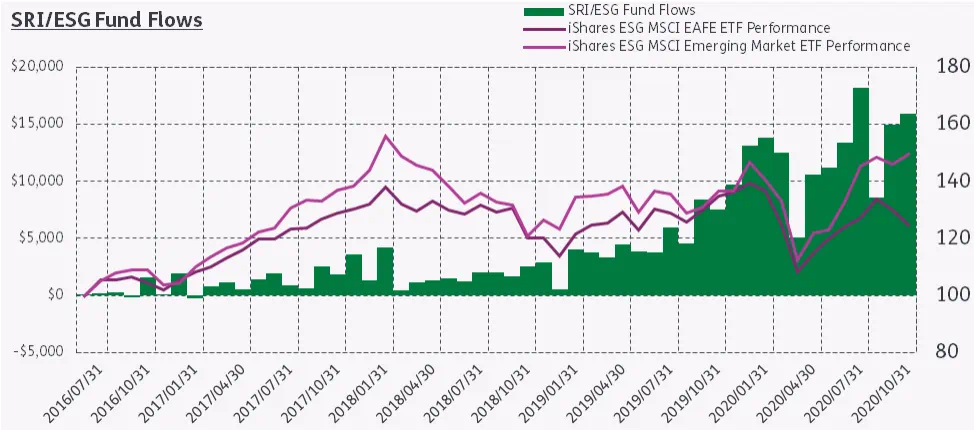

Unlike some of other ‘hot’ asset classes, such as Chinese equity and debt where strong retail flows and limited information makes it difficult to determine the relationship between flows and performance, there is a clear correlation between monthly SRI/ESG fund flows and the performance of the EAFE/EM benchmark.

If we compare current flows (in % of AUM terms) and future performance, there tends to a negative correlation (see Chart 2 below). If we compare concurrent flows and performance, they show a 40% and 45.92% correlation for EAFE and EM respectively.

Chart 2 – SRI/ESG Fund Flows vs Benchmark Performance

This surge in flows raises the issue of crowding – the building up of assets and flows in a still narrow corner of the overall market. And, with a new president-elect in the US who made ESG goals a central part of his campaign, this space is likely to get more, not less, crowded in the next four years.

This means that navigating this segment of the market profitably requires investors to side-step – or harness – this crowding.

Breadth over depth

In their 2002 paper, Chen, Hong and Stein [1] discussed ownership’s dispersion impact on security prices. The crux of their findings is that assets held by a broad number of owners perform better, and with less volatility, than assets where ownership is concentrated.

Based on these findings, EPFR’s Stock Flows dataset allows us to run a simple strategy based on the breadth of ownership for stocks with ESG credentials that are listed in the S&P 500 index.

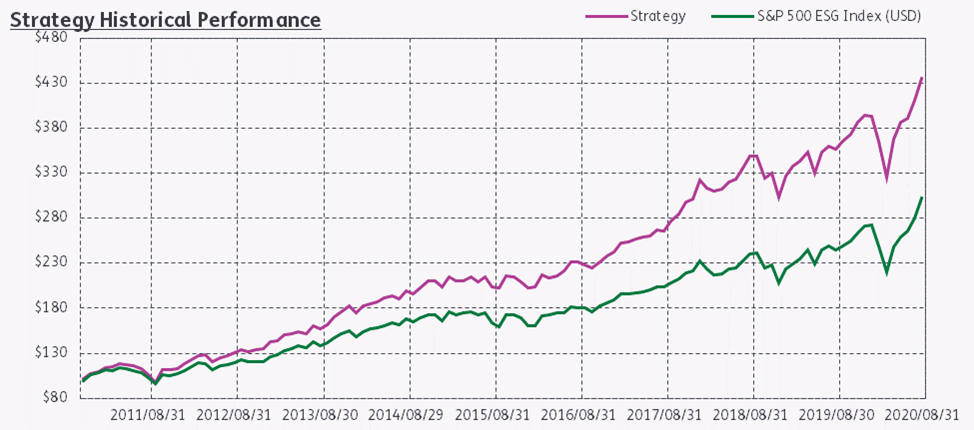

The strategy runs by identifying, buying and holding the top 20% most widely held ESG-compliant securities included in the S&P 500 index. The strategy rebalances on a monthly basis, and our back test suggests it would have returned 335% over the past 10 years versus the 201% gain recorded by the benchmark (see Chart 3 below).

Chart 3 – Strategy Historical Performance

We believe ESG will continue to see strong investor interest over the next few years. As more money in search of ESG assets floods into the market, using alternative data to navigate this corner of the market becomes essential.

In this short piece, we have illustrated one simple way that alternative data can help to avoid the negative effects of crowding and generate alpha.

Did you find this useful? Get our EPFR Insights delivered to your inbox.