Faced with rising geopolitical risk and globalization in retreat, investors showed little appetite for diversified exposure going into the final week of October. While Japan Equity Funds posted their biggest inflow in over seven months, flows into China Equity Funds rebounded and India Equity Funds extended their longest inflow streak since April 2003, a host of diversified fund groups posted outflows. Among them were Global Equity and Bond Funds, Europe Regional, Latin America Regional and Asia ex-Japan Regional Equity Funds, and both Global Emerging Markets (GEM) Equity and Bond Funds.

It was also another tough week for the major multi-asset fund groups, with Balanced Funds posting their biggest outflow in exactly a year and another $1.5 billion flowing out of Total Return Funds.

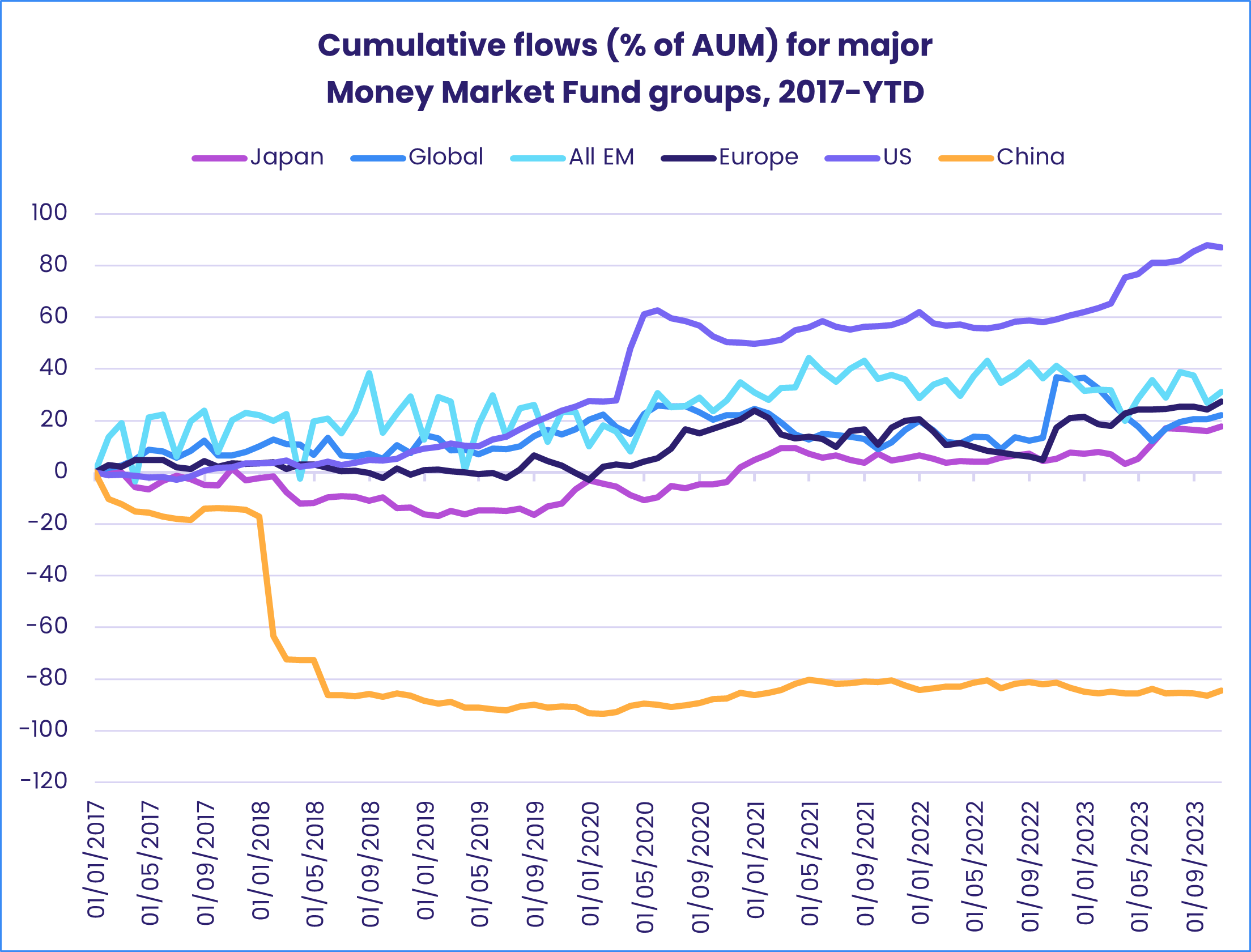

With risk appetite remaining at a low ebb, investors gravitated to cash and cash equivalents. Cryptocurrency Funds posted their biggest weekly inflow since 2Q22, Gold Funds snapped a 21-week redemption streak and Money Market Funds absorbed a collective $29 billion.

Overall, investors pulled a net $871 million from Alternative Funds during the week ending Oct. 25 while Equity Funds surrendered $2 billion and Balanced Funds $5.7 billion. For the second week running Bond Funds collectively absorbed $2 billion.

At the single country and asset class fund level, Poland Equity Funds chalked up their biggest weekly inflow in over a decade, flows into Finland Equity Funds hit an eight-week high and Australia Bond Funds extended an inflow streak stretching back to late April. High Yield Bond Funds extended their current run of outflows to six weeks and $16.5 billion, Mortgage-Backed Bond Funds absorbed over $1 billion for the second week running and money flowed out of Municipal Bond retail share classes for the 19th time in the past 20 weeks.

Emerging markets equity funds

Although flows to major Asia ex-Japan Country Fund groups held up during the fourth week of October and appetite for exposure to emerging markets dividend payers remained strong, EPFR-tracked Emerging Markets Equity Funds ended the week with their third outflow quarter-to-date as the diversified Global Emerging Markets (GEM) Equity Funds chalked up their 13th consecutive outflow and redemptions from retail share classes hit their highest level in over a year.

Flows into China Equity Funds bounced back, helped by anticipation of additional borrowing to fund infrastructure projects. Foreign-domiciled China Equity Funds, however, experienced net redemptions for the 13th time since the beginning of August. The latest EPFR Sector Allocations data shows technology and materials allocations at year-to-date and 21-month lows, respectively, while the average allocation to energy stocks is at its highest level since early 4Q19.

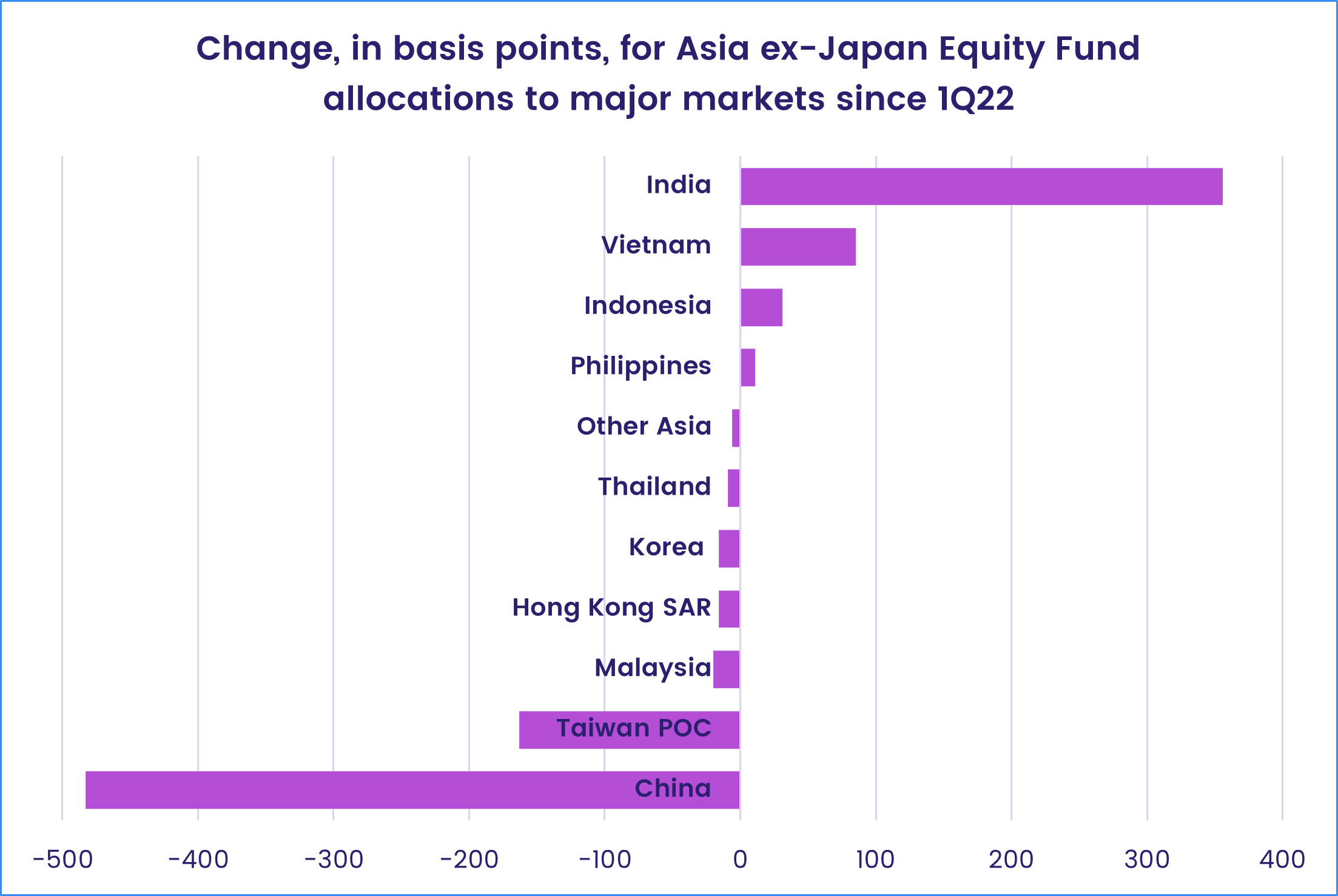

Among the diversified Asia ex-Japan Regional Equity Funds, China is the market that has seen the biggest cut in its average weighting since the beginning of last year. India and Vietnam have been the main beneficiaries, although their higher allocations have been offset by the fact this fund group is mired in a 29-week outflow streak.

In spite of the tension created by Israel’s latest clash with Hamas, which chased more money out of dedicated Israel, Turkey and Saudi Arabia Equity Funds, strong flows into Emerging Europe Regional and Poland Equity Funds helped EMEA Equity Funds post the biggest inflow since early September.

Latin America Equity Funds recorded their fifth outflow over the past eight weeks as investors pulled over $100 million out of Brazil Equity Funds and redemptions from Mexico Equity Funds climbed to a seven-week high. With mixed earnings reports to digest, a strong US dollar and a looming general election in Argentina to navigate, and key inflation reports coming down the pike, investors took a step back from this asset class going into late October.

Developed markets equity funds

Some solid third quarter earnings reports from US companies that were accompanied by positive guidance provided some respite from the headwinds, ranging from US Treasury yields in the vicinity of 5% to the threat of wider conflict in the Middle East, which have buffeted developed markets equity in recent weeks. But EPFR-tracked Developed Markets Equity Funds still ended the latest week with their third consecutive outflow as redemptions from Europe, Global, Canada and Pacific Regional Equity Funds narrowly offset flows into Japan, US and Australia Equity Funds.

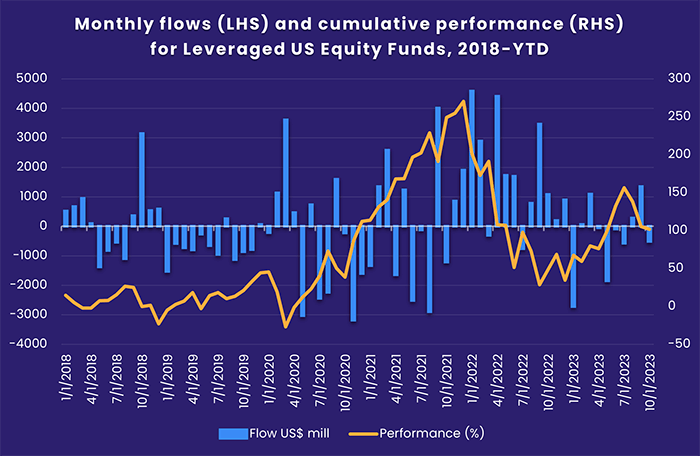

For the second week running US Equity Funds posted a collective inflow that represented 0.004% of their AUM. Large and Small Cap Blend ETFs accounted for the bulk of the week’s inflow as, for the third week running, actively managed funds in all of the major style and capitalization buckets posted outflows. Also experiencing redemptions, for the second time in the past three weeks, were US Leveraged Equity Funds. Funds with 2x leverage mandates posted their biggest outflow since mid-2Q20.

While US Equity Fund flows were measured in millions, Japan Equity Funds attracted over $2.5 billion – a 31-week high – with both foreign and domestically domiciled funds recording inflows. A decent start to the 3Q23 corporate earnings season and word that the government intends to cut taxes have added to the tailwinds enjoyed by Japanese equity this year.

Money continued to leak out of Europe Equity Funds ahead of the European Central Bank’s Oct. 26 decision on interest rates. The ECB kept rates on hold while signaling they could stay at current levels for some time. That will keep the pressure on a Eurozone economy struggling to avoid recession, with recent leading indexes offering little hope. At the country level, Austria Equity Funds posted their 35th straight outflow, Norway Equity Funds extended their longest redemption streak since 4Q11 and Switzerland Equity Funds chalked up their eighth inflow of the past nine weeks.

The largest of the diversified Developed Markets Equity Fund groups, Global Equity Funds, saw outflows hit a 44-week high with both Global and Global ex-US Funds surrendering over $1 billion. Funds with socially responsible (SRI) or environmental, social and governance (ESG) mandates saw money flow out for the sixth week in a row, the first time that has happened in over a year.

Global sector, industry and precious metals funds

Higher-for-longer oil prices and faith in the promise of artificial intelligence (AI) shaped flows to EPFR-tracked Sector Funds during the week ending Oct. 25, with Energy and Technology Sector Funds absorbing large sums of fresh money while most of the other major groups struggled.

The inflows for Energy Sector Funds in the latest week were the largest since March of last year, and came ahead of earnings reports from US and European energy giants such as BP, Exxon Mobil, Chevron and Shell. With wars in Ukraine and Gaza, clean energy initiatives and supply cuts by Russia and Saudi Arabia casting shadows over oil and gas supplies, investors are penciling in higher profits in the quarters ahead even with slower economic growth.

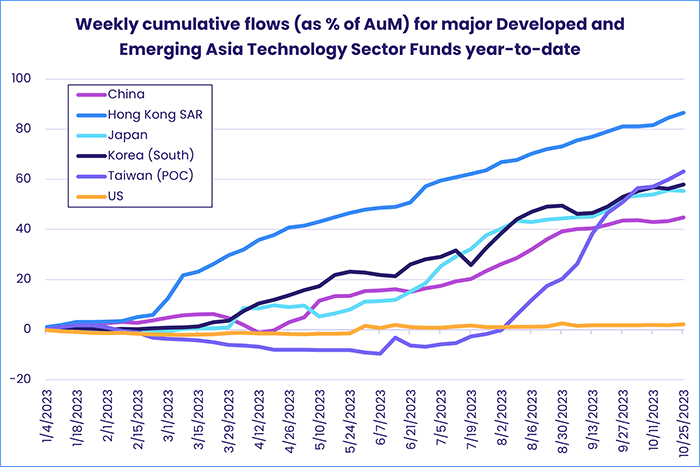

After a brief two-week blip, flows into Technology Sector Funds rode well-received earnings from Microsoft and Metaverse to an eight-week high of nearly $2 billion. At the fund-level, two semiconductor-mandated funds accounted for over $500 million of the headline number as leading producers of memory chips in US (Western Digital) and Japan (Kioxia) look to strike a deal. While US-dedicated funds brought home most of the money, China, Taiwan (POC), Hong Kong and South Korea Technology Sector Funds have seen generally persistent inflows. Semiconductor Funds enjoyed a 13-week high inflow and Robotics & AI Funds a 20-week high.

Gold Funds, a group that consists primarily of physical gold & derivatives funds, posted their first inflow in nearly five months. Equity Gold Funds – which provide a view of gold miners & mining – also posted inflows that snapped their four-week redemption streak. Despite this boost, Commodities/Materials Sector Funds suffered their fifth consecutive outflow.

Investors also pulled money from Infrastructure and Industrials Sector Funds. For the latter, it was the biggest outflow in 22 weeks. Drilling down, Construction Funds extended their outflow streak to seven weeks, Transportation/Shipping Funds posted their largest redemption since mid-3Q22 while Aerospace & Defense Funds reported a third straight inflow.

Consumer Goods Sector Funds saw another outflow above the $1 billion mark as the total surrendered during the past five weeks hit almost $5 billion. The funds with the largest inflows this week were a mixed bag of discretionary, staples, retail, construction, alcohol and livestock breeding.

Bond and other fixed income funds

EPFR-tracked Bond Funds heading into the final week of October posted their 39th inflow of the year-to-date as flows into funds with sovereign mandates continue to trump redemptions from Corporate Bond Funds. The latest week saw all Sovereign Bond Funds absorb nearly $9 billion while more than $4 billion flowed out of corporate funds.

Emerging Markets and Yield Bond Funds again found themselves on the wrong side of this tug-of-war between yield hunger and the desire to reduce risk, as both groups were hit with redemptions in excess of $2 billion which lifted the combined total for the past six weeks over the $28 billion mark.

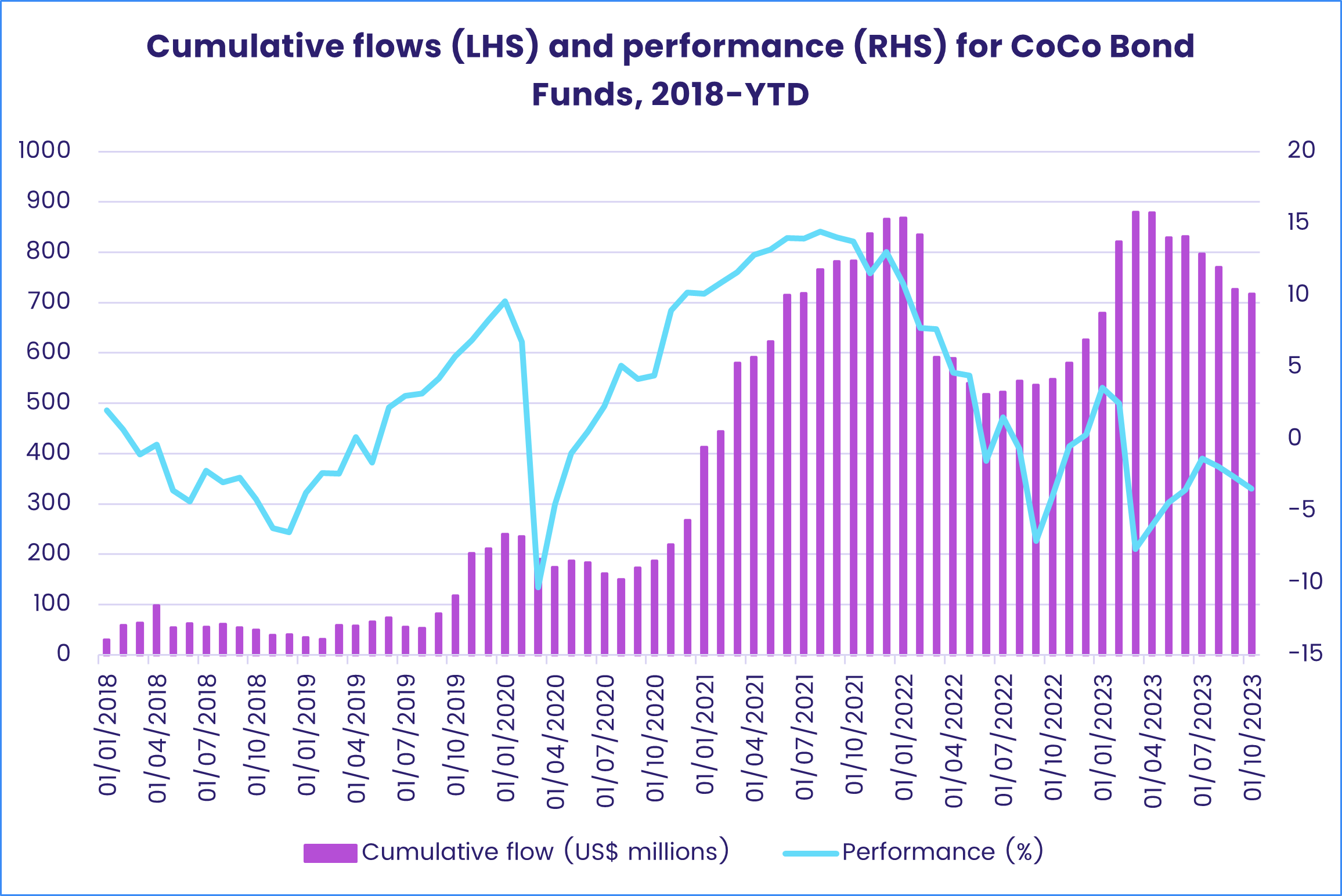

Investors sent a more ambiguous signal when it came to financial sector debt. Bank Loan Funds have recorded inflows during 15 of the past 18 weeks. But Contingent Convertible (CoCo) Bond Funds, which invest in debt issued to bolster European banks’ capital buffers, chalked up their fourth consecutive outflow.

US Bond Funds ended the latest week with their fourth straight inflow and 42nd year-to-date. Flows into US Sovereign Bond Funds were the biggest since mid-March, and Long Term Sovereign Bond Funds posted their biggest inflow since EPFR started tracking them in 1Q07. This contrasted with signals from the primary market, where a five-year, $52 billion issue was met with lackluster demand with dealers absorbing nearly a fifth of the issue.

The US remains by far the biggest single country allocation for Global Bond Funds, accounting for 43% of the average portfolio. Appetite for this group is at a low ebb, with the latest redemptions the biggest since the third week of March.

Emerging Markets Bond Funds remain under pressure from higher US and European interest rates, high-profile Chinese corporate defaults and weaker global growth prospects. The group last posted an inflow in late July and retail redemptions during the latest week hit their highest level since mid-2Q22. At the country level, Thailand Bond Funds chalked up their 11th straight outflow and China Bond Funds their 18th in the past 20 weeks while Czech Republic Bond Funds extended an inflow streak stretching back to early April.

Flows to Europe Bond ETFs so far this year are some $3 billion larger than flows into mutual funds. But ETFs share of the overall assets for all Europe Bond Funds is only 13%, up modestly from 10% at the end of 2018.

Did you find this useful? Get our EPFR Insights delivered to your inbox.